At present, a global energy crisis has punctuated the need and benefits for a much-faster scaleup of more affordable and less hazardous energy sources. No thanks to the unprecedented Russian invasion of Ukraine last year, food, energy, and other kinds of commodity prices seem to be reaching for the skies, advertently straining African economies that are still reeling from the aftereffects of the coronavirus pandemic.

Speaking of COVID-19, the outbreak effectively reversed the progress made to increase access to modern and sustainable energy, an objective enshrined in the United Nations’ SDG7. Home to nearly 800 million people with no access to any form of electricity, Sub-Saharan Africa is choicelessly the first on the unforgiving chopping block.

Moreover, Africa is smack in the middle of global climate change, facing the more severe consequences despite being the least responsible region for the looming catastrophe. With just one-fifth of the world’s entire population, the continent accounts for less than 3 percent of the world’s energy-derived CO2 emissions and is the region with the lowest emissions per capita.

Water stress, littler food production, more extreme weather occurrences, environmental pollution and low economic conditions are the right condiments for regional instability and mass emigration.

In view of correcting these abnormalities, clean energy transition holds vast opportunities for the social and economic development of Africa. As such, there is an essential question mark on how the continent is leveraging cleantech to achieve said transformation.

As of May 2022, countries accounting for more than 70 percent of the world’s CO2 emissions were committed to reaching net zero emissions by 2050. 12 African countries, which represent more than 40 percent of the continent’s cumulative C02 emissions, have similar mid-century goals.

Ultimately, these ambitions are indirectly setting a new course for the continent—where nearly all nations have subscribed to the Paris Agreement on Climate Change—to leverage technology in accelerating clean energy transition.

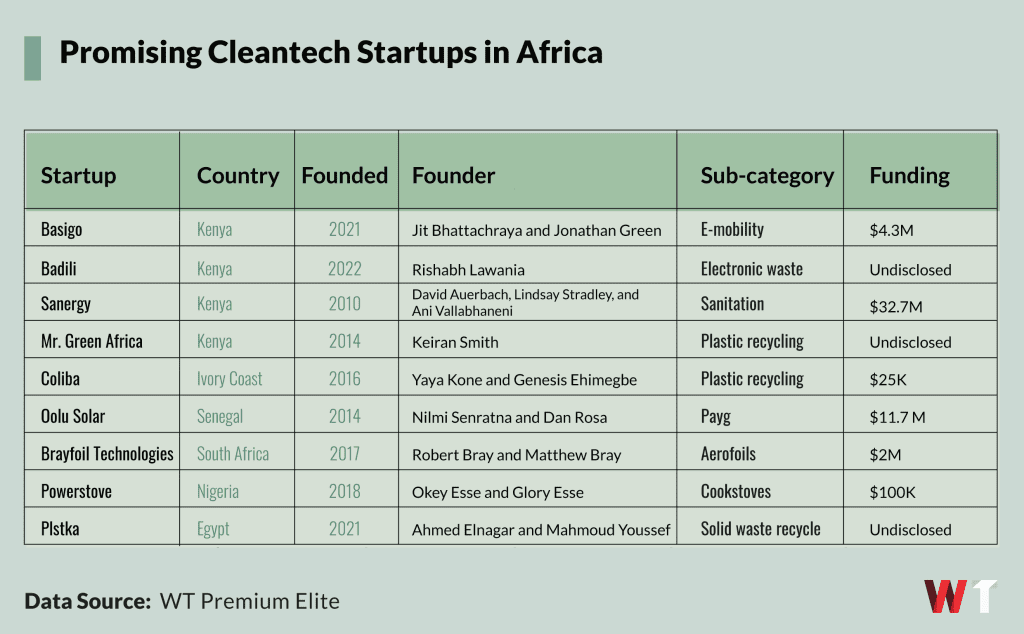

To showcase momentum in the sector, WeeTracker curated an index of some of the most promising startups driving cleantech adoption in Africa, most of which are newer companies with interesting business models backed by some high-profile investors.

Basigo

A Kenyan company that debuted in November 2021, BasiGo’s key innovation is a battery subscription service that separates the cost and charging of EV batteries from the cost of the bus. This allows customers to buy an electric bus for the same cost as a diesel-powered one.

The service uses the “pay-as-you-drive” model to enable operators to pay per kilometer, ultimately giving them a more reliable, affordable, and convenient way of moving people around. In the long run, BasiGo creates a much-needed opportunity to significantly reduce carbon emissions.

BasiGo, which is an amalgamation of Basi, a Swahili word for bus, and the English verb “Go”, plans to start selling locally assembled electric buses with parts purchased from Chinese EV maker, BYD Automotive. The buses will have 25 and 36-seater capacities and be capable of covering some 25 kilometers on daily trips.

To back these ambitions, BasiGo raised USD 1 M in pre-seed last November and closed a seed round of USD 4.3 M in February this year to accelerate its clean-energy mass transit vehicles. Its investors include Novastar Ventures, Moxxie Ventures, Nimble Partners, Spring Ventures, Climate Capital, and Third Derivative.

Badili Africa

About 35 percent of Kenyan consumers prefer buying second-hand smartphones over new ones. Nevertheless, safe, reliable, and legitimate options do not exist to do so; stolen, fake, counterfeit, and even dysfunctional devices are rampant in the market, creating a distrust setback for the sector. As such, most used phones mostly end up as solid waste, causing havoc to the human-inhabited ecosystem.

Badili Africa has created a plan to solve these challenges in Kenya, however with a longer-term continental perspective. The startup sources, repairs, and refurbishes used phones locally to resell them, essentially with a 12-month warranty. Its mission is not only to help consumers find affordable smartphone options and equally resell their used devices but also to help reduce the burden of electronic waste in the East African country.

Customers can buy refurbished phones for half the price of a new one, sell older ones instantly at incomparable prices and trade their existing devices for better options. The e-commerce or reverse commerce service offers these devices in 27 retail stores across 6 Kenyan cities, including Nairobi, Eldoret, Naivasha, and Nakuru, among others. Its trade-in services are accepted by Samsung and other well-known brands in the local market.

In May 2022, Artha India Ventures (AIV), Ashok Kumar Damani’s family office, made an undisclosed pre-seed investment in Badili, marking its first in Africa and eleventh on the international front. Uncovered Fund, Grenfell Holdings, Niche Capital, SOSV, Rajesh Sawhney, and Ritesh Malik also participated in the round.

Sanergy

Also based in Kenya, Sanergy is [basically] a waste management company launched by a group of former IT students in 2010 to franchise sanitation units throughout urban slums in Nairobi by providing an efficient and cost-effective alternative to sewers.

With the aid of black soldier flies, it gathers organic waste and human excreta deposits from sanitary toilets across Nairobian slums and converts them into insect feed, organic fertilizer, and biofuel. Sanergy opened its first organic recycling plant in Nairobi in 2015 and has since 2021 been operating the largest insect feed factory in East Africa.

Some of the processed material (KuzaPro) can also be used as livestock feed; Sanergy’s circular economy approach partly ensures that more farmers will have easier access to the products needed to accelerate food production. Presently, the business operates over 5,000 toilets across 11 informal settlements in Nairobi, serving more than 140,000 dwellers.

The company connects and improves its network through two mobile applications alongside mobile money, data collection, and street mapping technology. Since waste management and farming productivity problems are not peculiar to Kenya, Sanergy plans to expand across the continent, starting with East Africa.

With investors such as the Japan International Cooperation Agency, Kepple Africa, Acumen, and Novastar, the company has raised USD 32.7 M across 10 rounds.

Mr. Green Africa

This Kenyan company specializes in converting plastic waste into high-quality PCR, often sold to the public as an alternative to virgin plastics. A circular recycling service, Mr.. Green Africa has formulated a tech-driven plastic collection model that connects informal waste workers, micro-entrepreneurs, and consumers into a formalized value chain.

The company owns a chain of trading hubs in Nairobi and Kisumu where it purchases plastics from waste collectors and conveys them to a manufacturing plant it also owns. At the plant, the plastics are processed and sold to plastic manufacturers, ultimately for use by large fast-moving consumer goods businesses such as Unilever.

Mr. Green Africa, while formalizing the plastics supply chain, creates jobs and relieves emerging as well as growing cities from plastic pollution. In 2021, it became the first-ever African waste management and recycling company to receive certification as a B corporation, which established the business as a leader in the recycling industry.

Through the utilization of ethically sourced and locally generated Post Consumer Recyclate, the Kenyan firm works closely with brand owners, helping them achieve their sustainable packaging goals. Backed by DOB Equity, Global Innovation Fund, the Dow Chemical Company, Water United Impact, Bestseller, Circulars Accelerator and the Minderoo Foundation, among others, Mr. Green Africa’s long-term objective is transforming trash into value in emerging areas, integrating and reinforcing a local circular economy.

Coliba

Also applying the circular economic model, Coliba looks to tackle the plastic waste conundrum in Ivory Coast by allowing users to earn everything from airtime to discounts on certain products through recycling. With a mobile application, the company tracks users’ bottle collection progress and dispatches agents for the same purpose.

It has developed a waste management and recycling platform with the aid of an innovative and interactive web and mobile interface tailored to connect households and businesses in the country with affiliated plastic waste collectors.

More than 5 million tonnes of waste are produced yearly in Ivory Coast, with less than half of them being collected and merely 3 percent being recycled. Meanwhile, 94 percent of those who participate in this economy are in the informal sector.

To solve these problems, Coliba offers not only formal employment opportunities but also provides easy solutions for households to earn from recycling waste. The bottles collected are cleaned, sifted, and processed into P.E.T pellets and flakes, which are sold regionally and internationally for plastic-derived merchandise.

The startup has created 50 jobs, has a female employment rate of 75 percent, and counts Greentec Capital, the GSMA Ecosystem Accelerator, and Dakar Network Angels as its investors.

Oolu Solar

Based in Senegal, Oolu is an off-grid solar firm with a West African focus; it has sold more than 60,000 solar home systems to customers in Senegal, Nigeria, Burkina Faso, Mali, and the Niger Republic. The Y Combinator-backed startup is said to be one of the first companies to scale the PAYG solar tech model in the region, successfully.

Oolu, as a word, means trust in Wolof, the most widely spoken language in Senegal. From that perspective, the company aims to provide sustainable energy solutions, as well as financial solutions, to the no less than 150 million people dependent on national grids in Francophone and Anglophone West Africa, doing so with solar electricity kits.

The Senegalese startup offers after-sales services and warranties on some of its financing plans. What’s more, its monthly and annual PAYG setup allows customers to spread their investments into the kits over a given period, either via mobile money or direct bank transfers, after which (payment completed) the company will relinquish ownership of the products.

Oolu, which has a 50 percent women workforce, raised its Series A of USD 3.2 M in November 2017 and closed its Series B round of USD 8.5 M in December 2020, both of which were equity investments. Barring YC, its investors include Persistent Energy Capital, Shell-seeded impact investor All On, Gaia Impact Fund, and DPI Energy Ventures, among others.

Brayfoil Technologies

This South African cleantech company has come up with a compliant build-up and aerofoil model that assume bird-like shapes for larger wind turbines and lower-cost energy. Through its unique research and design, the South African firm has been able to develop as well as apply state-of-the-art technology to increase efficient clean energy access.

Working with corporate clients and research institutes, Brayfoil applies morphing technology to the design, test-running, and production of products in renewable energy as well as other industries. It caters to ventures utilizing clean energy systems like wind turbines, ultimately helping them reduce their energy costs using biomimicry-compliant structures.

After partaking in South Africa’s OceanHub Africa Accelerator, the company gained more international recognition as one of the participants of Katapult Ocean, which has over 100 portfolio companies across 35 nations and no less than USD 50 M in assets under management (AUM).

Brayfoil Technologies’ technology, which has been incubated by the Innovation Hub’s Climate Innovation Center, is fostered by global patents, more than USD 2 M in grant and equity funding, and a team of experienced engineers. The company is also part of Hello Tomorrow’s Top 100 companies in deep tech.

Powerstove

Incorporated in 2018, Powerstove combines sustainable resources with tech-driven innovations to create a versatile and affordable renewable energy solution for cooking. The Nigerian company converts non-recyclable paper, wood, and agricultural by-products of various plants into biomass pellets to fuel efficient, and no-smoke cookstoves.

These stoves can produce up to 50 watts of continuous power, generating just about enough energy to charge phones, and cameras and keep (rechargeable) lights on. They are equipped with IoT systems that come with pre-programmed and reprogrammable computer chips which control fans and electricity supply. To control these functions, the stoves transfer data over 2G and 3G networks via input sensors and output components.

This way, the Nigerian company claims to be the first and only clean cookstove in the world built with onboard IoT units. The shelf life of a single stove is a minimum of 5 years, and, in addition to cooking, each can charge battery-based electronic appliances in the home. While generating electricity, the stoves cook 5 times faster and allow users to monitor and control the cooking on a mobile application.

Clean Cooking Alliance, Africa Startup Initiative, Jua and Fund a AFR100-backed Powerstove’s offering is beneficial to the continent, where a substantial amount of households still rely heavily on traditional means of cooking, which are not only unarguably effective but also immensely contributed to household air pollution and, in the long-term, health issues. Per the WHO, this kind of pollution annually causes 4.3 million premature deaths.

Plstka

Plstka offers a mobile application that leverages a B2B-IoT supply chain model for waste management, helping users earn the most out of the solid waste they produce. The app allows for the swapping of solid waste for discounts and coupons from various everyday services like food, beverage, healthcare, and transportation.

Equally, customers can use their rewards to buy market items at discounted or lesser prices. The application, which was launched in early 2021, also [now] includes an in-game experience known as the Plstka Profitable Competition, wherein users compete with one another in raising more consciousness about the environment’s wellbeing.

The Egyptian firm aims to acquire some 1,500 tonnes of market waste in the country’s Delta region, representing USD 3 M of the total market size and covering over 100,000 households looking to get the most out of their generated trash and foster a cleaner and more habitable environment.

In early December 2021, Plstka raised an unspecified amount of seed funding from Alexandria Angels Network with a matching fund from Hivos, to build its user base and expand beyond Delta to other parts of Egypt.

With Africa at the epicenter of renewable energy adoption as well as climate change, it more than imperative to invest in more innovative and sustainable solutions that will help not just the continent, but also the world at large, make the most of cleantech’s exalted advantages.