In Africa, many agritech startups are developing businesses to solve the problems smallholder farmers face. These challenges are numerous and significant, including crop damage from natural disasters, high food wastage due to supply chain inefficiencies, and limited access to financial services. According to a report by the United Nations, Nigeria has the highest “per capita food waste rate” in Africa, estimated at 40% to 50%.

Many agritech startups begin their business from a single point in the agricultural supply chain. For example, they set up marketplaces that connect farmers (sellers) and companies (buyers). In the past few years, many startups that began as marketplaces pivoted their business to agricultural supply chains, such as cold storage and cold storage vehicles to prevent waste of farm products, or companies that manufacture processed farm products.

Zowasel, a Nigerian agritech startup, is one such company that comprehensively addresses the issues faced by smallholder farmers.

Jerry Oche was born into a farming family in northeastern Nigeria, and before founding Zowasel, he ran a crowdfunding business for small farmers. The crowdfunding business model was to sell the harvested crops and return the profits to investors, but it did not work out. The main reason was that small-scale farmers did not have appropriate sales outlets and could not sell their products at appropriate prices.

To solve this problem, Jerry founded Zowasel in 2017 as a marketplace business where farmers (sellers) and companies (buyers) could trade at an appropriate price. Over the years, the company started providing production guidance to farmers, selling inputs such as fertilizers and agrochemicals at lower prices than market prices, supporting opening bank accounts, etc.

Currently, in cooperation with Mitsubishi Corporation (MC) Nigeria, the company is implementing a farm machinery rental business for smallholder farmers and conducting a demonstration experiment of a credit-scoring business in cooperation with the Japan International Cooperation Agency (JICA).

A One-Stop Solution to the Challenges Facing Small Farmers

In order to provide an end-to-end solution to smallholder farmers, Zowasel has its main business is spread across 5 key verticals

(1) Marketplace (increase in profits and reduction of food loss)

(2) Crop cultivation education (improvement of cultivation knowledge)

(3) Introduction of farm machinery (production efficiency improvement)

(4) Credit scoring (improving access to finance)

(5) Traceability (visualization of distribution channels)

Currently, the company has a network of over 2 million smallholder farmers and about 5,000 sales partners. The agritech’s activities have expanded to many states in Nigeria. Its sales partners include major companies such as Olam, an agricultural general trading company headquartered in Singapore, Promasidor, based in South Africa, and Ireland’s Guinness.

In addition to providing fertilizers, seeds and guidance on appropriate cultivation & harvesting methods, the introduction of agricultural machinery by the startup has greatly improved productivity. Furthermore, Zowasel has removed the middlemen (usually 2 to 5 companies) from the supply chain, creating a win-win situation for farmers.

Now the farmers can sell at better prices, and companies can purchase farm products at lower prices. As a result, small farmers who have business relationships with Zowasel have seen their profits increase by an average of 30%.

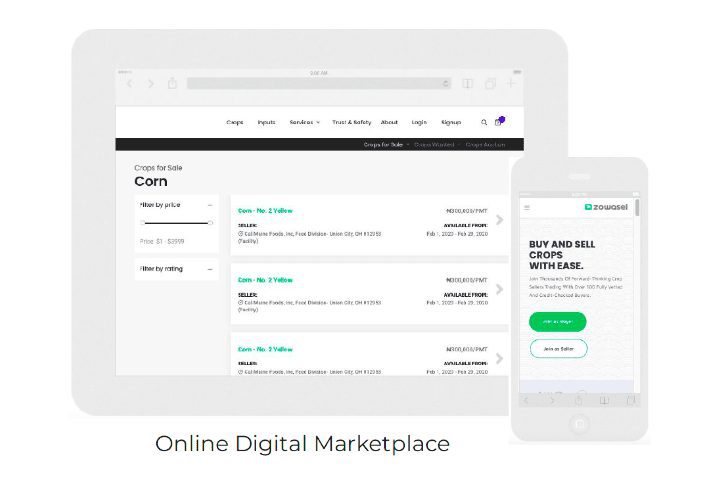

Marketplace

Zowasel provides an online trading platform that connects small-scale farmers with companies and enables them to buy and sell at appropriate prices.

There are three major challenges faced by small-scale farmers when buying and selling agricultural products: (1) lack of understanding of appropriate market prices, (2) lack of sales channels, and (3) logistics for transporting agricultural products.

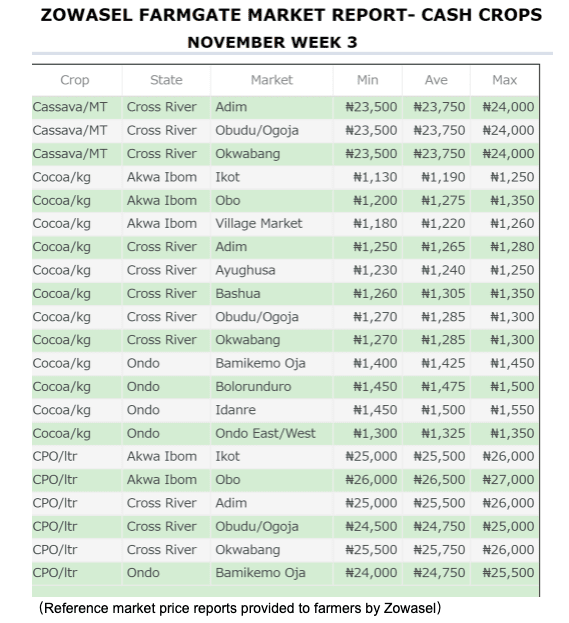

Zowasel researches and provides farmers with weekly reports of market prices for each agricultural commodity by region. The price list (below) shows the market prices of cassava and cocoa by region as surveyed by Zowasel.

When selling their produce, farmers determine the selling by themselves or with assistance from Zowasel, if needed. Every product undergoes quality inspections by Zowasel and is then entered into the online platform. By matching these data with the requirement entered online by the company (buyer), the transaction is concluded at a price that benefits both parties while eliminating the middleman. The final transaction price is determined through negotiations between the seller and buyer.

Another feature of the system is the use of mobile money to streamline payment. It is inefficient for both parties to travel great distances to make cash payments for sales. Since many smallholder farmers do not have bank accounts, Zowasel also assists them in opening bank accounts.

The company also provides logistics services after the transaction is completed, allowing customers to safely transport fresh products by hiring a carrier in partnership with Zowasel.

In addition, Zowasel has set up offices in each region to provide support to farmers who do not own cellphones & thereby, cannot use online trading and payment systems.

Education on crop cultivation

Lack of uniformity in crop production and inconsistent quality & quantity are other challenges faced by smallholder farmers. In most cases, the problem is due to ‘inexperience’ in cultivation techniques.

Zowasel provides free education to smallholder farmers on the cultivation of each crop, storage after harvest, and cutting fertilizer costs. It also updates current crop sales market trends and helps farmers grow their farming businesses.

The company offers 24-hour customer support, where farmers can call and talk to experts about commodity market trends and ways to improve their businesses.

Agricultural machinery rental business

Many smallholder farmers in Nigeria have difficulty purchasing agricultural machinery owing to their low incomes, and much of their farming is still done manually. As a result, the yield of harvest remains low.

On the other hand, the number of farmers leaving farming in Japan is increasing due to the ageing of the farming population. Many farmers are transferring or scrapping their farm machinery, and many unused, used farm machines are available in Japan. In addition, pre-owned machinery in Japan used for the cultivation of small fields meets the needs of smallholder farmers in Nigeria.

Therefore, in order to improve agricultural productivity through the diffusion of agricultural machinery to smallholder farmers in Nigeria, Zowasel and MC Nigeria have started a demonstration experiment of an agricultural machinery rental business in Nasarawa State. A total of four machines, an Iseki tractor, a Kubota combine harvester, and two hand-pushed rice transplanters manufactured by Kubota and Yanmar, were imported from Japan to provide rental services to farmers. This rental business, which started this year, is going well. Rental demand for agricultural machinery is strong, and the reservation list is full of requests from farmers.

Mr Makoto Saito, CEO of MC Nigeria, said, “Through the demonstration test, we are measuring the impact of agricultural machinery on farmers’ productivity and income and analyzing the economic rationale for the agricultural machinery rental business. If we can introduce a business-oriented agricultural machinery service, the Nigerian agricultural market will change dramatically. The potential is enormous.”

However, there are issues to be addressed in the farm machinery dissemination and rental business, such as (1) setting prices that farmers can afford, (2) appropriate maintenance, and (3) securing spare parts in case of breakdowns.

Mr Kisho Miyamoto, JICA Rice Extension Specialist, says, “Farm machines with simple functions that are popular in Southeast Asian countries like Thailand and Indonesia are more suitable for Africa. There is room to verify whether high-performance products for the Japanese market are better suited for the dissemination of agricultural machinery to small farmers in Nigeria or whether simpler, less expensive agricultural machinery with simplified performance used in Southeast Asia is more suitable for Nigeria.”

Another issue is whether the market is large enough to be a viable business in terms of securing spare parts in case of breakdowns. The key to building such an ecosystem is to first distribute a large number of agricultural machinery in the market. As the number of used agricultural machinery in circulation increases, more distributors would come up offering genuine spare parts, thereby growing the market. However, another challenge could follow with the distribution of non-genuine spare parts in the market.

Credit Scoring

Many small-scale farmers in Nigeria have low credit ratings and have difficulty utilizing bank loans and guarantees for business transactions. Most deals on the spot are in cash, making it difficult for the farmers to secure large sums of money to expand their businesses. Banks and other financial institutions are often reluctant to provide loans to small farmers, owing to the cost of access to remote and distant areas.

On the other hand, in addition to access to data on crop sales, purchases, and farm machinery rentals, Zowasel has extensive information on farmers’ personalities, family relationships, and farmland through its efforts to provide farmers with guidance on production methods. This data could be effectively utilized as credit data, especially since MC Nigeria and Zowasel are engaged in the farm equipment rental business

To add more meaning to the data, JICA and Office for Nigerian Digital Innovation (ONDI) launched the “Project for Improving Access to Finance and Livelihoods of Small-scale Farmers” in July 2022 in collaboration with Mitsubishi Corporation Nigeria and Zowasel. The project is an initiative to bridge the gap between financial institutions and small-scale farmers to solve the problems of both parties. This is part of JICA’s “Project NINJA (Next Innovation with Japan)” initiative to promote collaboration between local startups and Japanese companies.

The project’s objective is directly to improve smallholder farmers’ access to finance, expand their businesses, and improve their livelihoods, and in the process, various issues faced by small-scale farmers are expected to be resolved.

For example, improved access to finance will allow them to use rented farm equipment more, and increased productivity will free up more of their free time, allowing them to start a side business in their spare time. Children who used to help with farming would be able to focus on their schoolwork. In addition, if the improved livelihoods allow for the purchase of a small private power generation system (solar home system, SHS), children can study even in the middle of the night when there is no natural light. For an individual farmer, not only the access to finance will improve, but many other social issues are expected to be solved through derivative effects.

Furthermore, when the income of small-scale farmers improves, Zowasel, which has close relationships with farmers, will be able to provide a wider range of products and services.

Traceability

The European Union (EU) is debating a new bill aimed at preventing deforestation and forest degradation. Under the bill, 14 commodities to be exported to the EU, including cocoa, coffee, soybeans, beef, and corn, will have to prove that they are not produced on land that has caused deforestation. Since Africa exports many agricultural products to the EU, and cocoa is one of Nigeria’s main exports to Germany, the Netherlands, Spain, Belgium, and other countries, there is concern about the impact of the bill.

Products that meet EU standards will be exported, while those that do not meet standards will be bought cheaply by other countries, potentially putting small farmers in developing countries at a disadvantage.

In anticipation of the proposed legislation, Zowasel is focusing on traceability to provide data on “where, when, by whom, and how the products it purchases were produced. The company is working with Barry Callebaut AG, a major Swiss company that deals mainly in cacao beans and chocolate products, to promote sustainable cocoa production in Nigeria.

Specifically, agricultural and sustainability experts will be dispatched to production sites to provide guidance to farmers on production, collection of farmland and crop data, as well as gender considerations, forest and environmental protection, and other issues. Barry Callebaut has also pledged to strengthen its support for cocoa cultivation to achieve carbon neutrality by 2025.

Jerry, CEO of Zowasel, said, “The EU bill could be detrimental to small farmers and companies that produce commodities that do not meet EU standards. We want to develop our business in a way that benefits both Nigerian farmers and the EU,” he said.

Strong relationship with farmers

Zowasel’s greatest strength is the direct and strong relationships with farmers that Jerry, CEO of the company, has built and the business he develops by leveraging these strong relationships.

Jerry’s relationship-building is solid and reliable. He spends many days in rural areas during the year, building strong relationships with government officials and town and village mayors in each state. He is very active in explaining the company’s business activities to farmers in the region, and after gaining the approval of smallholder farmers, he onboards them onto the company’s platform.

Zowasel has established 45 crop centres in Nigeria. These centres not only work as service centres of the company but also as a place for farmers to enjoy conversations and build relationships. I visited Ondo State, Nigeria, a cocoa-producing region, in May this year and Nasarawa State in November and was able to experience firsthand the close relationship between the company and the village heads and farmers in these areas.

The business model of Zowasel is time-consuming and human-centric, and the speed of business expansion is slower than that of software startups such as FinTech. However, the company’s strength lies in its “access to small farmers,” a solid network of small farmers that Jerry has built through his visits.

Such a tight-knit network is highly attractive to foreign companies that want to do business with small farmers in Nigeria but do not have a network. Some European companies, such as MAS Seeds of France, are already using the company’s network to conduct demonstrations to adapt their fertilizers, seeds, and other inputs to the Nigerian environment.

How it looks like going forward

Agritech startups targeting small-scale farmers in Africa are increasingly offering one-stop services from production to sales. These services range from agricultural technology guidance, provision of necessary materials at low cost, farm equipment rental services, trading at appropriate prices on online platforms, AI-based credit scoring businesses, and mobile money utilization and financial access services.

Depending on the business model, future agritech businesses targeting smallholder farmers are likely to approach the role of a platform that sells a wide range of offerings, including daily necessities. The business can be more robust by building strong relationships with small-scale farmers and collaborating with more companies to create a value chain.

In business for the BOP (low-income earners/small-scale farmers), collaboration among other industries centred on companies with sales access to customers will be key.

Mr Susumu Yuzurio, Chief Representative of JICA’s Nigeria Office, commented, “While JICA’s business mainly involves government agencies as counterparts, startups have the advantage of building close relationships with end-users. As with the credit scoring project, we would like to actively seek linkages between the startups’ strengths and existing JICA projects in areas such as agriculture and health in order to implement projects with greater impact and solve social issues,” he said.