The fraudster who cleaned out one Nigerian fintech last week is probably applying for an account at another one today. And unless someone says something, he’ll probably get it.

This is the paradox Lanre Ogungbe has been staring at for years. As CEO of Prembly (formerly Identitypass), a compliance and identity verification company serving 800 businesses monthly, he’s watched the same patterns repeat. A fraudster hits Platform A, gets flagged, vanishes, then reappears on Platform B using the exact same phone number, the exact same ID, the exact same playbook.

“They use the same tactics on another platform because you were quiet about it,” Ogungbe tells WT. “We’ve seen this multiple times play out, enabled by your silence.”

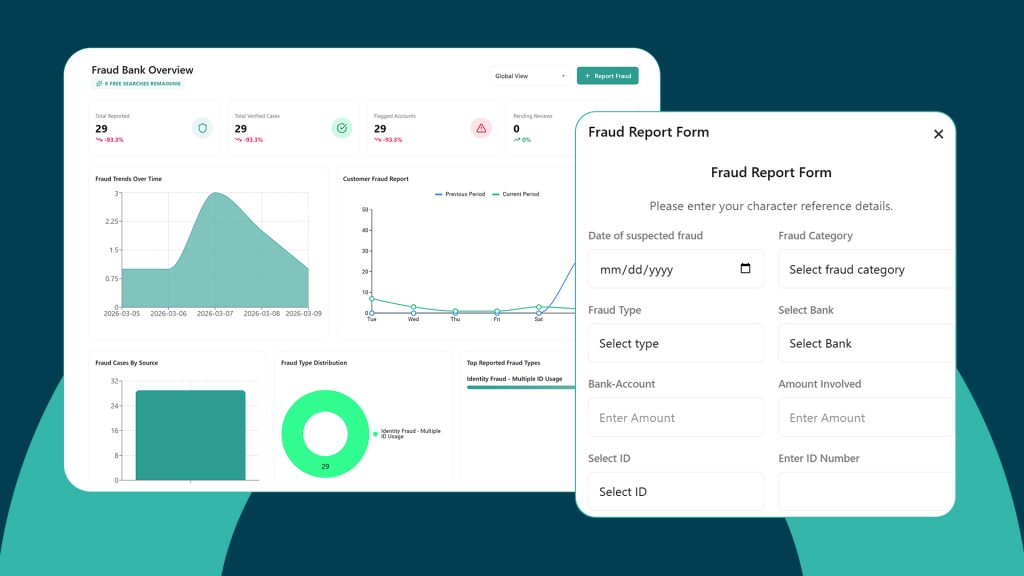

This week, Prembly is launching FraudLens, billed as Africa’s first effective open-source fraud intelligence bank.

The idea, to get financial institutions to actually share data about who’s ripping them off, though simple in theory yet complicated in practice, is starting to find traction.

How it actually works

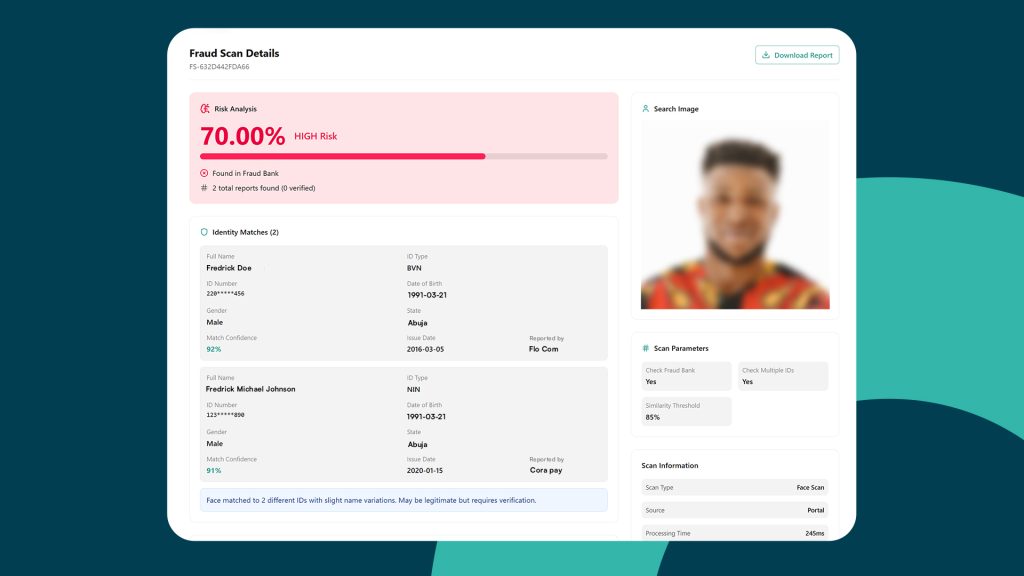

Prembly’s FraudLens has two faces. The public side is a real-time dashboard showing fraud trends, patterns and prevalence; fraud awareness made accessible, so to speak.

Anyone can see that this week, 451 fraud events were reported, that Niger state is showing unusual activity, that Lagos leads in attempted compromises.

The private side is where the actual work happens. Verified, regulated businesses that subscribe to Prembly’s platform get access to a shared database.

When they onboard a new customer, the system flags if that phone number, that ID, that device fingerprint has been reported by other institutions. The business doesn’t have to act on the information—it can still approve the customer—but at least it knows what it’s walking into.

Crucially, reporting isn’t free-for-all. Every submission requires vetted evidence. Internal approval. A paper trail.

“We can’t just have somebody submit something false,” Ogungbe explains. “If you wrongly claim a consumer committed fraud, there’s a liability process. There’s a retrieval process if we made a mistake.”

Will rivals actually share?

On the surface, we like to imagine fraud as Hollywood hacking; hooded figures breaking through firewalls in dark rooms. But sit with Ogungbe, and he’ll tell you the truth is both simpler and more disturbing in that the system is designed to stay quiet.

“We don’t do a lot of documentation of the events that happen,” Ogungbe says. “When fraud happens, we are meant to document it so that we can prevent it. But the issue is that when you document, it comes with panic.”

This is the knot at the centre of Nigeria’s fraud problem. Document a major fraud event, and consumers will withdraw their money. Banks collapse. It’s played out in the past, the generations that watched banks go under in the 1990s carry that trauma. So institutions stay silent. Fraudsters get documented nowhere. And the same person who cleaned out one fintech walks into the next one and does it again.

“Fraud really works when data is hidden,” Ogungbe explains. “We’ve seen the same ID reported as fraud by a particular fintech, and the same person used the same ID to go to another platform and commit the same type of fraud. That could have been prevented if the other person had said something had happened.”

The obvious question—and Ogungbe has heard it enough to pre-empt it—is why competitors would cooperate. Banks spend millions fighting each other for customers. Why hand over intelligence that might expose their own weaknesses?

Ogungbe’s answer is that they already do. Just not publicly.

The Bank Verification Number system is owned by the banks. Nigeria Inter-Bank Settlement System is private, owned by the banks. Compliance officers from every major financial institution meet monthly and share information, Ogungbe points out. As it turns out, the competition that plays out in marketing campaigns doesn’t extend to the back rooms where fraud is discussed.

“From a public market perspective, it has to appear as though there’s a war between everybody,” the Prembly CEO says. “But what really happens at the back end is different.”

Credit bureaus already share default data by law. Fraud data, he argues, is the logical next layer, and the infrastructure simply didn’t exist before.

Traditional systems from NIBSS, the Central Bank and the police force weren’t built by KYC companies. He maintains that they lacked the verification technology, the biometric integration, the big-data analysis that the Y Combinator-backed startup has spent years building.

The fraud that lives in the infrastructure

When Ogungbe runs through how money actually gets stolen in Nigeria, the Hollywood hacking narrative barely registers. The real damage is systemic, he asserts; fraud is built into the systems themselves.

He discovered he personally had over 15 bank accounts opened in his name that he knew nothing about. Created during his NYSC days, when banks flooded camps with sign-up drives. Created by branch managers chasing targets, created using his information without his knowledge.

“You trace it down, it comes from a manager somewhere that insists that for the branch to stay open, you have to open 50,000 new accounts in a community of less than 100,000 people,” he says. “How do they do that? They use the same information to open multiple accounts.”

This is what Prembly’s system is designed to catch. Not the lone hacker in a dark room, but the organised operation running the same synthetic ID across five platforms in the same week.

The weaponisation concerns

Any database of alleged fraudsters raises uncomfortable questions. Who decides someone is a fraudster? What happens when a business gets it wrong? Could this become a de facto blacklist with no appeal process?

Ogungbe acknowledges the risks. The system is currently restricted to businesses with proper compliance structures, specifically to prevent weaponisation. Individuals can’t report other individuals; that loophole stays closed until safeguards are stronger.

“Can it be weaponised? Yes. Have we been able to close the loop from an individual perspective? No. That’s why we’re not releasing that to the public,” he says.

For now, only the statistics are public. The private details stay with verified institutions, and every flagged entry comes with evidence. If a business reports someone for chargeback fraud, it needs to show the transaction. If it’s identity fraud, it needs to show the ID mismatch.

The cat-and-mouse reality

Ogungbe doesn’t pretend this ends fraud. Fraudsters will adapt. They’ll find new loopholes, new infrastructures to exploit, new ways to weaponise AI and social engineering. The game is cat-and-mouse, and the mice are motivated.

“What that does is it makes them ask more questions,” he says. “It makes them have heightened security. If somebody can go through the stress and beat everything you’ve put in place, then the amount they’re going after is worth it. For those cases, you pursue them.”

The goal, he says, isn’t perfection but making fraud harder. It’s ensuring that the person who hit one platform can’t simply walk into the next one unchallenged. It’s introducing consequence into a system designed for speed above all else.

“If we can reduce fraud losses by half or more in five years, that’s a winning streak for us,” Ogungbe says.

The trust question

Ask Ogungbe what success actually looks like, and he doesn’t point to dashboards or press releases. He speaks of the Opay rider who accepts a transfer without waiting to confirm. The POS operator who trusts that the money actually moved. The consumer who stops checking their banking app with dread.

“That is what we’re tracking,” he says. “Create more trust within the consumer space.”

For now, trust is still in short supply. The EFCC recently dropped numbers that should give everyone pause: NGN 18.7 B stolen, more than 900,000 victims, one customer operating 960 accounts in a single bank, and NGN 162 B (~USD 114 M) in suspicious cryptocurrency transactions with no oversight.

A system built for speed discovering, belatedly, that silence has a cost. And it would soon become clearer whether shared intelligence arrives in time to matter, or whether the fraudsters have already moved on to the next loophole.