South Africa is recording the highest share of deepfake-driven fraud in Africa, with 22% of cases involving AI-generated impersonation, according to the 2026 Digital Identity Fraud Report by identity verification company Smile ID.

The findings show that nearly nine in ten rejected verification attempts in the region are now linked to AI-assisted impersonation and spoofing during biometric checks.

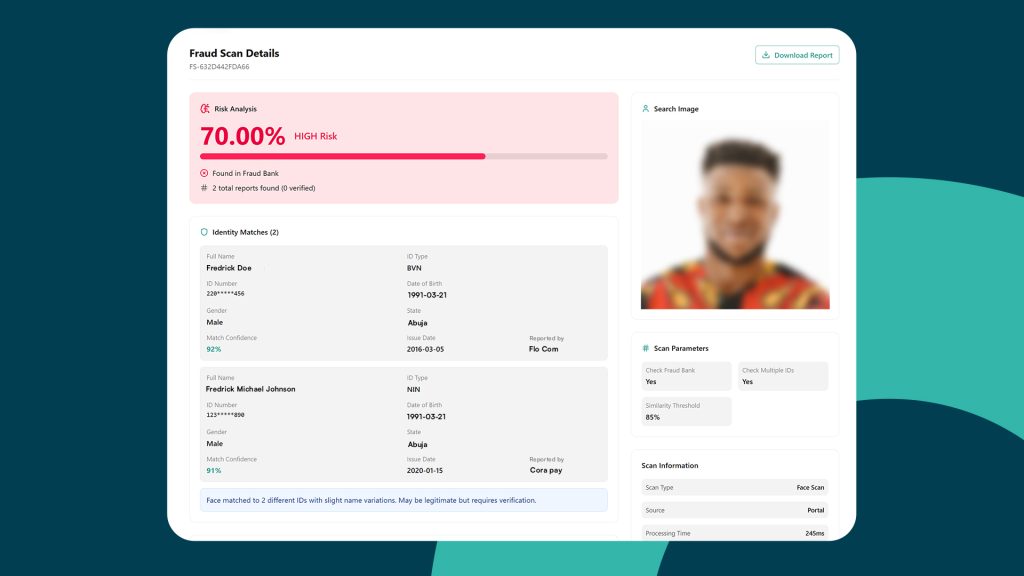

Fraudsters are no longer focusing on fake documents. Instead, 47% of cases involve no-face-match impersonation, where the person verifying cannot be linked to the claimed identity, suggesting large-scale use of stolen personal information. Another 40% are spoofing attacks designed to defeat liveness detection and facial recognition systems.

The shift reflects how radically affordable AI tools have changed the game for criminals. What once required technical skill can now be done with free or cheap generative AI software that creates realistic fake videos, clones voices from social media clips, and generates synthetic faces that fool verification systems.

Smile ID detected more than 100,000 injection attacks per month in 2025, where fraudsters bypass device cameras entirely by feeding synthetic or pre-recorded media into verification systems through emulators and virtual cameras.

South African regulators and companies are already seeing the impact. The Financial Sector Conduct Authority has warned about deepfake videos impersonating high-profile figures, including President Cyril Ramaphosa and Patrice Motsepe, to promote fake investment opportunities. Momentum Group’s financial director, Risto Ketola, was impersonated in a scam involving an invite-only WhatsApp group in June last year, using a photo taken from LinkedIn.

The threat extends beyond individuals to businesses. Richard Ford, group CTO at Integrity360, says criminals now scrape audio from TikTok, Instagram, or Facebook to clone voices using inexpensive AI tools, then call employees pretending to be executives in distress. Finance administrators receive WhatsApp voice notes that sound exactly like their financial directors requesting urgent payments to new suppliers, exploiting what Ford calls a “subservient reflex” to obey senior figures.

“Fraud is no longer a ‘KYC’ problem — it is a continuous cybersecurity challenge,” Mark Straub, CEO of Smile ID, said. “AI enables fraudsters to operate at unprecedented scale and sophistication.”

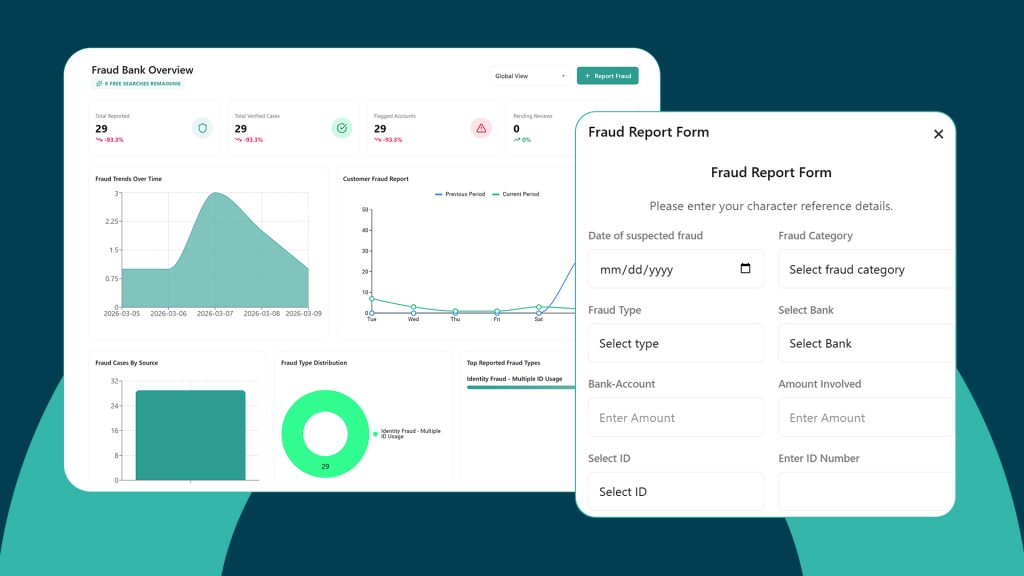

Authentication-related fraud attempts are now five times more common than fraud at the point of account onboarding, Smile ID found from analysing anonymised data from more than 200 million identity verification checks it conducted in 2025, spanning 37 industries in over 35 countries.

Attackers are no longer focused on breaking in, the report suggests. They operate inside verified accounts, targeting login flows, password resets, device changes, and high-value transactions. Once inside, AI automation lets them reuse verified biometrics and move funds across platforms at scale.

Smile ID found more than 160,000 fraudulent verification attempts in a single month traced back to just 100 facial identities, with some faces appearing over 12,000 times across multiple platforms. Another case saw attackers use the same identity for more than a thousand account registration attempts within 30 minutes.

AI expert Johan Steyn says voice cloning, face swaps, and synthetic identity profiles have increased exponentially over the past year because the tools have become cheap, accessible, and convincing. He advises companies to treat identity as a continuous risk system rather than a one-off verification step, using device and behavioural signals to detect anomalies and requiring out-of-band confirmations for sensitive changes like beneficiary additions or high-value payments.

The 22% figure for South Africa is the highest in Africa, but the problem is continent-wide. In West Africa, 65% of fraud attempts involve biometric spoofing, BusinessDay reports. Across Africa, organisations face an average of 3,153 cyber attacks per week, 60% higher than the global average, according to Check Point Software Technologies.

“Effective defence now requires network intelligence: By leveraging these privacy-preserving indicators throughout the customer lifecycle, we enable real-time adaptation. Identity has entered the security era, where ecosystem-wide protection is essential to safeguarding the individual,” Straub said.

Feature Image Credits: Terovesalainen/Adobe Stock