Thank you for signing up for our free newsletter. By entering your email id you agree to receive our free newsletter and other promotional communication.

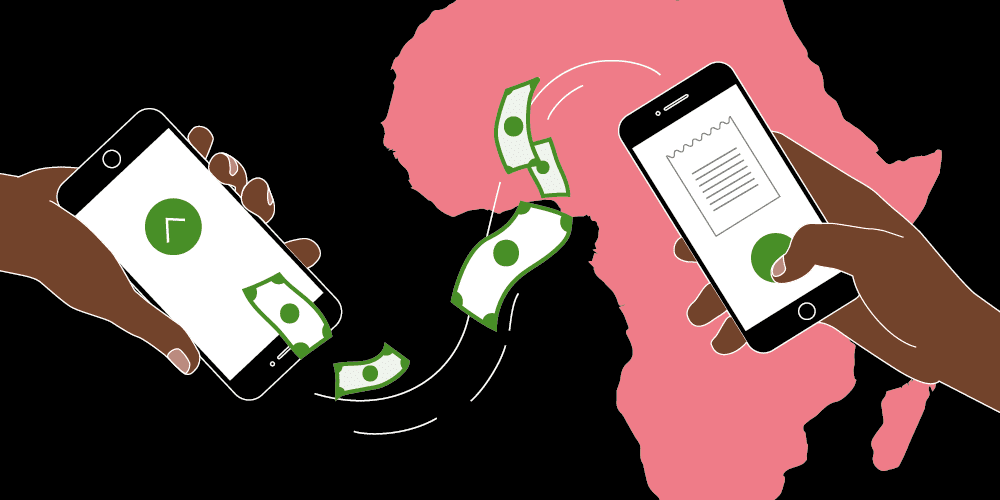

African Fintechs Jostle As Cross-Border Payments Serve Up ‘Biggest Opportunity’

By Henry Nzekwe

|

June 1, 2026

For most Africans, sending money across a border is often a hassle marked by high fees, slow transfers, and funds that disappear for days. But that pain is now driving one of the continent’s biggest business opportunities.

A new industry ranking reveals that sub-Saharan Africa is on the cusp of a cross-border payments boom as it’s becoming the continent’s biggest fintech opportunity. Five African companies: Flutterwave, M-PESA, MTN’s MoMo, Mukuru, and Onafriq, have made the 2026 Cross‑Border Payments 100 list by FXC Intelligence, standing alongside global giants like Visa and PayPal.

For a construction worker in Lagos whose brother in London sends USD 200.00 home every month, or a trader in Nairobi buying goods from South Africa, or a student in Ghana paying tuition in Canada, each transaction bleeds value. International transfers can cost 8% or more, and funds can take days to arrive, or never arrive at all.

African fintechs are fixing this by building direct connections between local mobile money wallets, banks, and global systems. Instead of a payment bouncing through three or four intermediary banks in New York or London – each taking a cut – these companies create shortcuts.

M-PESA, Kenya’s mobile money giant, moves more than USD 1 B daily across Africa. MTN’s MoMo processed over USD 500 bB in transactions last year alone. Onafriq links one billion mobile wallets across the continent.

A new shortcut

More quietly, a new tool, stablecoins, is changing everything. These are digital dollars that live on a phone. As it requires no bank account and no middlemen, a Nigerian freelancer paid by a US company can receive stablecoins instantly and convert them to local cash within minutes.

Sub-Saharan Africa recorded roughly USD 205 B in stablecoin-linked on-chain value from July 2024 to June 2025, a 52% year-over-year surge. In Nigeria, 95% of survey respondents said they would prefer to receive payments in stablecoins rather than in naira.

Big companies are notices. Deel, the global payroll giant, launched stablecoin salary payouts in May after processing USD 250 M in crypto payouts last year. Earlier this year, Onafriq integrated Conduit’s stablecoin infrastructure, using USDC for treasury settlement to bypass the USD 5 B annual friction of correspondent banking.

Africa’s diaspora sends home more than USD 100 B every year, more than all foreign aid combined. Yet much of that money still travels through slow, expensive channels.

The continent’s cross‑border payment market could more than triple to USD 1 T by 2035, according to projections. That is why global players like Binance, Tether and Visa are also on the FXC list, scrambling for a slice.

For ordinary Africans, the competition cannot come soon enough. Cheaper, faster money transfers mean more cash in pockets, more business done, and fewer sleepless nights waiting for a transfer to clear.

Feature Image Credits: Openway Group

Once‑Beloved Fintech Brass Absorbed Into Paystack MFB After Two-Year Rescue Bid

By Staff Reporter

|

June 1, 2026

Two years after a high‑profile rescue by a Paystack‑led consortium, Nigerian business banking startup Brass has ceased operating as an independent entity, with its operations now absorbed into Paystack Microfinance Bank in a move that closes the chapter on the once high-flying fintech as a standalone entity.

Founded in July 2020 by Sola Akindolu and Emmanuel Okeke , who met while working at Kudi and Paystack respectively, Brass raised a USD 1.7 M round in October 2021 that drew backing from Flutterwave CEO Olugbenga “GB” Agboola and Paystack co‑founder Ezra Olubi. The startup built a digital banking platform that offered business accounts, payroll tools, expense management and cash‑flow tracking, positioning itself as a modern banking layer for African SMEs.

But by October 2023, cracks began to show. Customers reported delays in processing withdrawals, sparking liquidity concerns across the ecosystem. In March 2024, Brass furloughed an unspecified number of its roughly 50 employees, with Akindolu citing “significant economic shifts” in a public statement. The delays continued for months, and ecosystem stakeholders worried that the collapse of a deposit‑taking fintech could trigger a wider bank run on digital financial services.

In May 2024, a consortium led by Paystack, with participation from PiggyVest, Ventures Platform, P1 Ventures and angel investors, acquired Brass for an undisclosed amount, replacing Akindolu and his founding team with new leadership. The acquisition ended months of speculation, though some investors raised questions about liabilities, with two sources describing a NGN 2 B (~USD 1.4 M) hole in the company’s balance sheet that Brass’s leadership could not account for.

On Monday, Brass announced that interested customers would be migrated into Paystack MFB before July 31, 2026, integrating its business banking operations into Paystack’s regulated banking infrastructure. “As we rebuilt and as our platform became more mature, something became increasingly clear: the next phase of our growth could not be achieved alone,” the company said.

Paystack, which was acquired by Stripe in 2020 for USD 200 million, absorbs Brass to deepen its expansion from payments processing into full‑stack financial services; a shift that began in January when it entered Nigeria’s banking sector by acquiring Ladder Microfinance Bank.

The integration also signals the maturity of Africa’s fintech market. After years of venture‑backed startups building overlapping products, consolidation is now accelerating as capital and regulation tightens.

Mobile Money Fees To Get Costlier As Kenya Pushes Digital Taxes, Operators Warn

By Staff Reporter

|

June 1, 2026

Mobile money users in Kenya could see transaction costs rise by up to 18.4% under proposed tax changes, industry players have warned lawmakers, potentially reversing years of hard-won gains in financial inclusion.

The warnings come from two of Kenya’s most prominent digital payments players—the operator of the dominant mobile money network, M‑PESA, and global card giant Visa—as Parliament considers the sweeping Finance Bill 2026.

Safaricom, which owns M‑PESA, appeared before parliamentarians to oppose a clause in the bill, which would slap a 16% value‑added tax (VAT) on digital payment platforms on top of an existing 15% excise duty already charged on mobile money transfers.

The telco calculated that the two levies would push the effective tax burden on an M‑PESA transaction from 15% to 33.4%, translating directly into higher costs for Kenya’s 51 million mobile money users. On a typical transaction, fees could climb by as much as 18.4%, the company said.

“What I’m foreseeing happening is us going back to instances where people would have money stuck underneath their mattresses,” Kiema Onesmus, KPMG East Africa Associate Director for Tax and Regulatory Services, told CapitalFM, warning that the shift could push users back to cash-based transactions.

Treasury Cabinet Secretary John Mbadi has defended the digital tax push. “The person who supplies ICT to enable payments is the one subject to VAT,” a Treasury official said, stressing that the levy targets platform fees, not the money being transferred directly.

But analysts and payment firms say that argument misses how mobile money works. Fees earned by PSPs come from user charges, they point out, and the additional 16% VAT will simply be passed on in the form of higher costs to the customer.

Visa has also stepped into the fray. The global payments company is tracking proposals to impose withholding tax on interchange and merchant service fees on every card transaction. Visa’s detailed modelling found that for a typical KES 10 K (about USD 77.00) purchase, a merchant currently receives KES 9.8 K. If the bill passes in its current form, that same merchant would receive just KES 9.768 K, a KES 32.00 (USD 0.25) hit on a single transaction.

The Kenya Bankers Association (KBA) has lodged formal opposition, warning that the compounding tax burden could push total digital financial transaction costs from 15% to 58.4%, potentially reversing the country’s celebrated status as a global leader in mobile money adoption.

The stakes are starkly illustrated by M‑PESA’s recent performance. The platform moved KES 41.68 T (USD 323 B) in the last financial year, with active merchants expanding 71% to 3.1 million. A meaningful hike in those transaction costs could dent a digital economy built on low‑cost, high‑volume transfers.

“The proposals, if they sail through as they are, will set us back way more, almost like a thousand steps,” Onesmus warned, urging a rethink of a revenue strategy that could ultimately shrink the very tax base it aims to expand

Africa’s Crowdfunding Agritech Woes Worsen In Collapse Of SA’s Top Platform

By Henry Nzekwe

|

May 29, 2026

For a heady few years, agritech crowdfunding was pitched as the answer to Africa’s agricultural financing gap, offering retail investors a chance to bankroll smallholder farmers while pocketing double-digit returns. After a cascade of high-profile collapses and a final liquidation order against South Africa’s once-popular agro-crowdfunding, Livestock Wealth, the model is now being written off as fundamentally unworkable.

The Gauteng High Court recently placed Livestock Wealth under final liquidation, ending an 18‑month‑long rescue bid and drawing a line under a platform that had once managed over ZAR 100 M (~USD 6 M) in assets. The ruling followed months of investor complaints over delayed withdrawals, with one stokvel claiming it was owed nearly ZAR 140 K despite receiving written repayment promises.

A two‑year Financial Sector Conduct Authority investigation concluded that the company had not broken financial services laws, noting that agricultural assets are not classified as “financial products” under South African law, but imposed administrative penalties for misleading conduct.

Livestock Wealth’s downfall mirrors a graveyard of similar ventures across the continent. In Nigeria, Farmcrowdy, once the poster child of digital agriculture, ran into trouble and pivoted away from crowdfunding in 2021 after regulatory pressures and market instability forced it to reinvent itself as a B2B agricultural service provider.

ThriveAgric, another Nigerian pioneer, survived a near‑fatal crisis in 2020 after hundreds of unpaid retail investors took their grievances online; the company restructured its operations, dropped public crowdfunding and now focuses on institutional partnerships and its Agricultural Operating System. Agropartnerships, reQuid and Farmsponsor have also folded or exited the crowdfunding business.

Regulatory ambiguity has compounded the problem. In Nigeria, the Securities and Exchange Commission’s belated foray into crowdfunding regulation failed to weed out unsustainable operators, while the Investment and Securities Act 2025 now imposes fines of NGN 20 M and up to 10 years’ imprisonment for promoting Ponzi schemes. The NFIU has warned of a surge in unregulated crowdfunding scams between 2022 and 2025, noting that fraudsters often masquerade as agricultural investment platforms.

The underlying economics are equally unforgiving. Agriculture in Africa faces a USD 65‑80 B annual financing gap, but venture capital expects fintech‑like returns that farming cycles cannot deliver. “Capital always follows the path of least resistance,” Lola Masha, partner at Antler, toldTechCabal earlier this year. “Agritech is hard. It’s a very different reality from fintech”. That mismatch, compounded by a 90% failure rate for Nigerian agritech startups within five years, has pushed investors toward infrastructure and energy.

The few survivors have abandoned the public‑facing crowdfunding playbook entirely. ThriveAgric now supports over 200,000 farmers through its digital operating system, working with institutional capital rather than retail investors. Farmcrowdy has repositioned itself as a food value‑chain and logistics partner. But for thousands of retail investors across Africa, it’s been a painful lesson discovering that crowdfunding agritech was an idea whose roots haven’t quite taken to the ground.

Africa’s Tech Leaders Turn From Startups To Factory Floors

By Henry Nzekwe

|

May 27, 2026

A unique USD 100 M philanthropic fund, backed by some of Africa’s most consequential tech founders, is betting that the continent’s startup economy has missed the trick chasing funding rounds instead of factory floors.

The Africa Jobs Fund (AJF), launched today by Wasoko founder Daniel Yu and counting Andela and Flutterwave co-founder Iyin Aboyeji among its senior advisors, is targeting large-scale formal job creation, a problem that venture capital has largely sidestepped.

“Persistent poverty is at its core a jobs problem,” Yu said. “Those same people, in the right job at home or abroad, could earn significant multiples of their income. AJF exists to back the companies that create those jobs and opportunities.”

Sub-Saharan Africa adds 15.4 million people to its labour force every year but creates only about 3 million formal jobs. By 2040, approximately 600 million of the world’s extreme poor are expected to reside on the continent. Meanwhile, nearly 9 in 10 workers remain in informal employment, such as street vending, gig work, and subsistence farming, with little income growth or social protection.

AJF’s thesis is deliberately targeting export manufacturing and international labour mobility, two sectors that have historically lifted countries out of poverty.

The logic is that a worker moving from subsistence agriculture to a factory job can increase productivity fivefold. The same worker securing a care or logistics role in a high-income country can see their annual income jump from roughly USD 2 K to USD 40 K or more. Yet these pathways remain blocked by high setup costs for pioneer manufacturers and predatory recruitment fees for migrant workers.

AJF aims to mobilise USD 100 M over five years to de-risk early-stage companies in both sectors with the goal of generating USD 50 B in cumulative income gains for African workers and doubling the lifetime earnings of at least 250,000 low-income individuals.

Unlike a traditional VC fund, AJF is a program of Renaissance Philanthropy, the nonprofit founded by former White House science advisors Tom Kalil and Kumar Garg, and includes former USAID Administrator Samantha Power as a senior advisor. With a focus on venture-style execution for social good, the fund aims to “bet early and activate the founders who can act on that thesis,” as Garg put it.

Yu, who built Wasoko into a B2B e-commerce platform serving over 150,000 informal retailers, said his experience taught him that “traditional businesses can be just as impactful — maybe even more so — than glitzy tech startups”.

This new chapter was signalled eight months ago when Yu announced he was stepping back from daily operations at Wasoko after the company’s merger with MaxAB. At the time, Yu said he was moving to India to focus on personal projects, including his role as board chair of Malengo, a nonprofit that facilitates international educational migration. His experience at Malengo, which helps low-income students move to Germany for university and work, directly influenced AJF’s labour mobility pillar.

Yu is not going it alone. The fund has recruited Ben Hyman, founder of the African recruitment firm Talent Safari, as Operating Partner.

Aboyeji, who has since pivoted to his own job-focused venture called Learn2Earn, a tuition-free, stipend-supported, 24-month programme that guarantees jobs for elite software engineers, struck a similar note having been tapped as an advisor. “African founders have shown they can build category-defining companies. The next decade is about building the ones that put millions of people to work,” he said.

A decade of venture capital has produced nine African unicorns and attracted billions in funding. But those companies, for all their innovation, have not moved the needle on mass employment. AJF represents a recognition that solving poverty may require less disruption and more manufacturing.

New Rules Targeting Foreign Capital Send Mixed Signals In African Tech

By Staff Reporter

|

May 26, 2026

For over a decade, venture capital has been welcomed into African markets with open arms as the missing ingredient for a tech revolution. This year, a cascade of new laws across the continent is sending mixed signals.

Ghana, Kenya, and Uganda have all advanced or enacted measures in recent weeks that tighten scrutiny on foreign capital, from ownership restrictions in strategic sectors to exit taxes and stringent disclosure rules. The cumulative effect is rattling investors and founders at a precarious moment for the continent’s startup ecosystem.

In Accra, a contradictory picture is taking shape. Last month, parliament passed the Ghana Investment Promotion Authority Bill, 2026, scrapping the notorious USD 500 K minimum capital requirement for wholly foreign-owned enterprises; a move hailed as a game-changer for tech founders.

But tucked into Section 37 of a draft National Information Technology Authority bill, not yet before parliament, lies a rule stipulating that licenses for cloud hosting, SaaS, data centres, or government digital partnerships would be reserved for entities “wholly owned by a citizen.”

“This directly threatens the foreign capital, partnerships, and expertise that fuel Ghanaian success stories,” says MacJordan Degadjor, a Ghanaian technology policy commentator, citing homegrown firms Hubtel and mPharma as examples of what is at stake.

Communications Minister Samuel Nartey George has defended the draft, saying there is “no intent to exclude ‘big tech'” and that the government aims to “proactively protect Ghanaian technology firms” to build local capacity. But concerns remain rife. Technology blogger Alfred warned the bill could “undo years of digital sector progress.”

Meanwhile, Kenya is widening its tax net. The Finance Bill 2026, tabled on May 25, proposes a 15% capital gains tax on offshore sales where shares “derive their value from Kenya”—a direct assault on the holding-company structures that foreign venture capital and private equity investors have used for years to exit without local tax liability.

The move is partly driven by high-profile disputes, including a KES 21 B (USD 161.7 M) tax demand tied to Tullow Oil’s offshore exit. But the Institute of Certified Public Accountants of Kenya (ICPAK) warns the amendment is dangerously broad. “As drafted, the provision may create Kenyan CGT exposure for offshore investor exits, capital raising transactions, group restructurings and internal reorganisations undertaken at holding company level,” the body told parliament.

“In most developed markets, this kind of tax is meant to stop profit shifting. The way it’s drafted in Kenya, it could tax legitimate internal reorganisations—a nightmare scenario for compliance,” said Robert Waruiru, Managing Partner at Ichiban Tax and Business Advisory.

In Uganda, President Yoweri Museveni signed the Protection of Sovereignty Bill into law on May 17, criminalising the promotion of “interests of a foreigner against the interests of Uganda” and requiring government approval for foreign-backed policy work. Rights groups warn the broad language could criminalise political opposition.

Crucially, the final bill amended an earlier provision that would have forced any Ugandan receiving foreign money to register as a foreign agent. The original text, which Bank of Uganda Governor Michael Atingi-Ego warned could trigger “economic disaster,” now applies only to funds received “for political purposes.” Remittances, USD 2.5 B in 2025, or 3.8% of of Uganda’s GDP, were spared, but the episode rattled diaspora and development partners alike.

The timing also brings concern amid a funding slowdown. Data from Africa: The Big Deal shows only 162 unique investors participated in startup deals worth USD 100 K or more between January and April 2026, a five-year low and a 26% drop from the same period in 2025. Total equity funding into African startups fell 13% in the first four months of 2026.

There are concerns that African governments are sending contradictory signals, seeking investments to build a digital future while simultaneously building legal walls to keep investors out.

Some local capital is stepping into the void. The Africa Finance Corporation launched a USD 100 M investment push this month aimed at reducing foreign dominance in startups.

“The challenge is no longer talent or innovation, but the shortage of long-term African institutional capital,” AFC President Samaila Zubairu said. Whether that will be enough to offset the regulatory chill remains an open question.

Kenya’s Boda Boda Riders Drive USD 2.9 M EV Charging Boom For State Utility

By Staff Reporter

|

May 25, 2026

Frederick Wanyonyi spent six years ferrying passengers through the lakeside city of Kisumu on a petrol-powered motorcycle, watching fuel costs slowly eat away his profits and his ability to support his family. Today, the 34-year-old rides an electric motorcycle supplied by Spiro Kenya, and his math has changed dramatically.

“Previously, I would spend more than KES 500.00 every day on fuel alone. Now I spend about KES 290.00 on battery swapping and I am able to save more money for rent, school fees and food,” Wanyonyi toldKenya News Agency.

Across Kenya, millions of informal transport workers like Wanyonyi are voting with their wallets. And their shift is quietly rewriting the earnings of the country’s state-owned utility.

On Thursday, Kenya Power announced cumulative revenue of KES 382 M (approximately USD 2.9 M) from electric vehicle (EV) charging over the past 34 months, as electricity sales to the e-mobility sector grew more than 113-fold between July 2023 and April 2026. Monthly EV charging revenue rose from KES 874 K (roughly USD 6.7 K) in July 2023 to a peak of KES 35 M (USD 271 K) in February 2026, according to the utility’s E-mobility Sales Growth Analysis Report.

The growth is being driven not by wealthy consumers in Teslas, but by the two-wheeled backbone of Kenya’s economy. Data from the Electric Mobility Association of Kenya shows the country had registered over 35,000 EVs by the end of 2025, up from just 796 units three years earlier, with two- and three-wheelers dominating the market. Riders report lower daily running costs, fewer mechanical breakdowns, and more predictable expenses compared to petrol alternatives.

For Kenya Power, which sources over 90% of its electricity from renewables, the e-mobility boom presents a rare strategic alignment as it grows electricity demand without expanding fossil fuel dependency. Under the utility’s e-mobility tariff, customers pay KES 16.00 per unit during peak hours and KES 8.00 during off-peak hours, incentivising overnight charging that helps balance grid load.

Yet infrastructure remains the sector’s Achilles’ heel. “When electricity goes off, business slows down because batteries cannot be charged,” said John Mark, who manages a battery-swapping station in Kisumu, pointing to a challenge that persists even as Kenya Power rolls out new charging stations from Voi to Nyali.

The utility plans to introduce more EV-friendly tariffs and expand its own electric fleet to 20 vehicles and 100 bikes by the end of 2026. But the real story is unfolding on the roads where hundreds of thousands of boda boda riders are making a calculation that requires no government subsidy.

Wanyonyi already did the math. “With these bikes, servicing is less frequent,” he said. “Maintenance has reduced considerably”.

Scaling with Confidence: The Importance of Reliable IT Infrastructure

By Partner Content

|

May 22, 2026

Growth is the goal of every ambitious business — but growth without the right infrastructure creates its own set of problems. Systems that worked adequately for a ten-person team begin to strain under the demands of a fifty-person organisation. Security gaps that were manageable at a small scale become serious vulnerabilities as the business becomes a more attractive target. Technology decisions made for short-term convenience create long-term technical debt that slows future progress. For businesses in San Antonio ready to scale with confidence, reliable IT support in San Antonio from Evolution Technologies provides the infrastructure foundation that makes sustainable growth possible.

The Infrastructure Inflection Point

Most growing businesses encounter an IT inflection point — a moment when the technology approach that served them well at an earlier stage is no longer adequate for where they are headed. This inflection point often arrives without warning, triggered by a system failure, a security incident, a compliance audit, or simply the accumulating weight of deferred maintenance and unresolved issues.

Recognising the inflection point before it becomes a crisis is one of the most valuable contributions a managed IT partner can make. By continuously monitoring infrastructure health, tracking capacity trends, and maintaining visibility into the organisation’s technology roadmap, a proactive IT partner can identify when current systems are approaching their limits and help the business make planned, strategic transitions rather than reactive, emergency ones.

Building Infrastructure That Scales

Scalable IT infrastructure shares several key characteristics. It is built on platforms and architectures that can grow with the business without requiring complete replacement. It is documented thoroughly so that new team members and support staff can understand and manage it effectively. It is continuously monitored so that capacity constraints and performance issues are identified before they become failures. And it is secured comprehensively, so that growth does not introduce new vulnerabilities.

Cloud-based infrastructure is particularly well-suited to growing businesses because it scales on demand — adding capacity as needed without large capital investments in hardware. Microsoft Azure, Microsoft 365, and other cloud platforms provide enterprise-grade capabilities that can be right-sized for businesses at any stage of growth, and can expand quickly as needs evolve.

The Hidden Cost of Infrastructure Neglect

Businesses that defer IT investment to preserve short-term cash flow often discover that the long-term cost of neglect far exceeds what proactive maintenance would have required. Ageing hardware fails at the worst possible moments. Unpatched systems become vectors for security breaches. Undocumented configurations slow down and make troubleshooting expensive. Technical debt accumulates until it requires a costly, disruptive remediation effort.

The businesses that scale most successfully treat IT infrastructure as a strategic investment rather than a cost to be minimised. They maintain their systems proactively, invest in security before incidents occur, and make technology decisions based on long-term value rather than short-term expense. This approach requires discipline and the right partner — but it pays dividends in reliability, security, and the ability to grow without technology becoming a constraint.

Security at Scale

As businesses grow, their security requirements grow with them. More employees mean more potential entry points for attackers. More systems mean more vulnerabilities to manage. More data means more valuable targets. The security approach that was adequate for a small team is rarely sufficient for a mid-sized organisation.

Evolution Technologies helps growing San Antonio businesses build security programs that scale with their operations — implementing controls that address current risks while establishing the foundation for more sophisticated security capabilities as the organisation matures. This includes endpoint protection across all devices, identity and access management that enforces least-privilege principles, network monitoring that detects anomalous activity, and incident response capabilities that minimise the impact of any breach that does occur.

The Partner Advantage

Scaling a business is demanding work. Leadership attention is a scarce resource, and every hour spent managing IT problems is an hour not spent on customers, products, and growth. The right IT partner removes technology from the list of things leadership needs to worry about — handling the day-to-day management, the proactive maintenance, the security monitoring, and the strategic planning that keeps infrastructure aligned with business objectives.

For San Antonio businesses with growth ambitions, Evolution Technologies provides that partnership — combining technical expertise, proactive management, and deep familiarity with the local business environment to deliver IT infrastructure that supports rather than constrains the journey ahead.

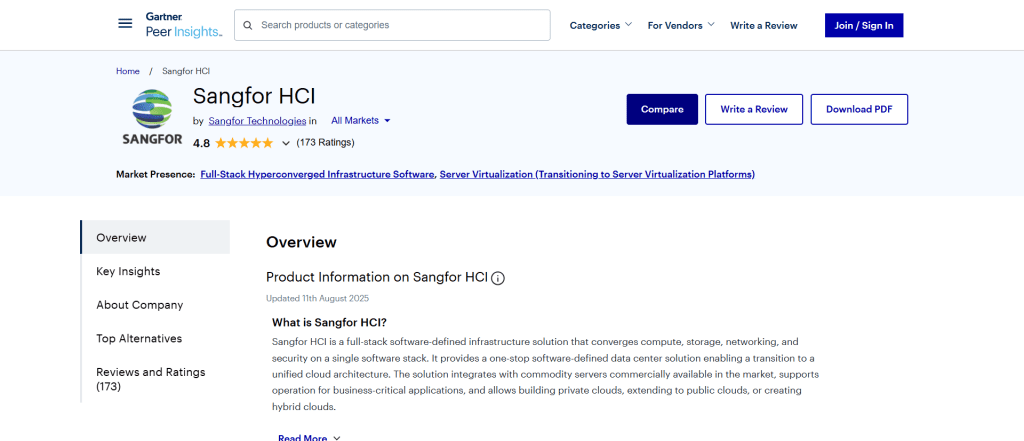

Smart Manufacturing in 2026: How Hyperconverged Infrastructure Enables Industry 4.0 Efficiency

By Partner Content

|

May 21, 2026

Walk into any modern manufacturing unit today, and the shift in how things operate is impossible to ignore. Machines do a lot more now; they talk, calculate, respond in real time, and production lines behave like synchronised systems.

That shift, quietly but decisively, is being powered by infrastructure decisions most people never see.

In 2026, the conversation around Industry 4.0 feels less theoretical, with the real question now being, “How efficiently do manufacturers digitise?” This is where HCI use cases for manufacturing become a practical discussion, and where providers like Sangfor have been steadily building relevance.

The Infrastructure Problem Nobody Talks About

Manufacturing innovation is generally framed around robotics, AI, or IoT. But whenever we scratch the surface, we see that legacy infrastructure struggles to keep up with the density and speed of modern data loads.

This is aggravated by systems that work in silos and allow latency to creep in.

Worse, with so many issues, maintenance becomes an operational burden.

The backend becomes more complicated with each new machine: traditional three-tier setups were never designed for this scale of convergence, and they fracture under pressure when real-time decision-making becomes unavoidable.

This gap explains why conversations around hyperconverged infrastructure keep surfacing as a necessity. To clarify, as compute, storage, and networking no longer operate independently, they converge into a single, software-defined layer.

Why Does HCI Make Sense in Manufacturing Environments?

Think about a factory floor that relies heavily on predictive maintenance: sensors constantly stream operational data from machines, which needs to be processed instantly to prevent failures. In such cases, a delay of even a few seconds can impact output, or worse, safety.

HCI simplifies that entire flow, as instead of routing data across fragmented systems, everything is processed within a unified framework. This leads to less latency, fewer failure points, and better scalability.

Some practical benefits tend to stand out, which are:

Centralised management across distributed factory environments

Faster deployment of new production applications

Built-in redundancy for critical manufacturing operations

Reduced dependency on specialised IT maintenance

These improvements directly translate into production uptime and cost moderation.

Real HCI Use Cases for Manufacturing that Teams Are Prioritising

This is where theory starts to transition into application.

When manufacturers evaluate HCI seriously, a few use cases repeatedly come up.

Smart Production Line Optimisation

Production lines today generate massive data streams. With HCI, that information can be processed closer to the source for immediate optimisation. So, instead of analysing performance later, adjustments happen in real time.

Edge Computing Integration

Factories rarely operate from a single location; multiple plants, warehouses, and edge nodes require synchronisation. HCI supports seamless edge deployments while maintaining central control. This means that manufacturers get consistency without sacrificing local responsiveness.

Disaster Recovery and Data Continuity

Downtime in manufacturing is not measured in hours but in financial impact per minute. To solve this, HCI creates built-in replication and recovery mechanisms that ensure operations bounce back quickly when disruptions occur.

Virtual Desktop Infrastructure for Factory Operations

Operators and engineers often need secure access to applications across locations, and HCI supports virtual environments that enable centralised, secure access. This reflects how HCI use cases for manufacturing are evolving; it’s less about infrastructure efficiency and more about operational resilience.

Why are manufacturers moving away from traditional infrastructure?

Manufacturers are moving away from traditional setups primarily due to scalability and speed limitations. With Sangfor solutions, HCI simplifies deployment and reduces system complexity, enabling manufacturers to respond faster to operational demands without redesigning their infrastructure.

The Role of Hypervisors in Modern Manufacturing IT

Another layer to this conversation that doesn’t get enough attention is virtualisation. More specifically, the ongoing debate around Type 1 vs Type 2 Hypervisor environments.

Type 1 hypervisors operate directly on hardware, making them better suited for mission-critical environments, whereas Type 2 hypervisors are more flexible but introduce an additional software layer that can increase latency.

Sangfor’s approach prioritises lean architecture and minimal overhead, aligning closely with the needs of high-performance manufacturing. After all, choosing the right hypervisor setup becomes part of a broader efficiency strategy rather than just a technical decision.

How does virtualisation impact factory performance?

Virtualisation improves flexibility, but poor implementation can slow systems down. Sangfor optimises this balance by integrating efficient hypervisor capabilities into its HCI platform. This enables manufacturers to maintain performance and scalability without trade-offs.

Industry Validation and Market Reality

When it comes to claims made by vendors holding up to real-world scrutiny and scenarios, nothing is more reassuring than great reviews on well-known peer-review platforms.

Date: May 13, 2026

Gartner and G2 are such platforms where users rate Sangfor highly for its HCI solution: 4.7 out of 5 on G2 and 4.8 out of 5 on Gartner for HCI implementations. This is a testament to operational outcomes across industries, which reduce uncertainty for those looking to invest in long-term infrastructure transitions.

An example of success was when Sangfor HCI was implemented to support PT JFE Steel Galvanising Indonesia’s Manufacturing Execution System, operating 24/7. Compute, storage, and networking were consolidated into a single platform for this, and the company achieved simplified infrastructure management.

What kind of results can manufacturers expect after adopting HCI?

Sangfor HCI solutions ensure that manufacturers experience improved uptime, faster deployment cycles, and simplified IT management. The overall production efficiency and reliability improve.

This is a Defining Year for HCI in Manufacturing

Smart manufacturing in 2026 is defined by ambition, and this depends heavily on how well underlying systems perform under pressure. With that, the rise of HCI applications in manufacturing reflects that manufacturers aren’t just adopting technology; they are choosing systems that enable them to recover more quickly and scale smarter.

Sangfor’s role in such a scenario feels less like that of a vendor and more like that of an enabler, as it quietly reshapes how infrastructure supports production.

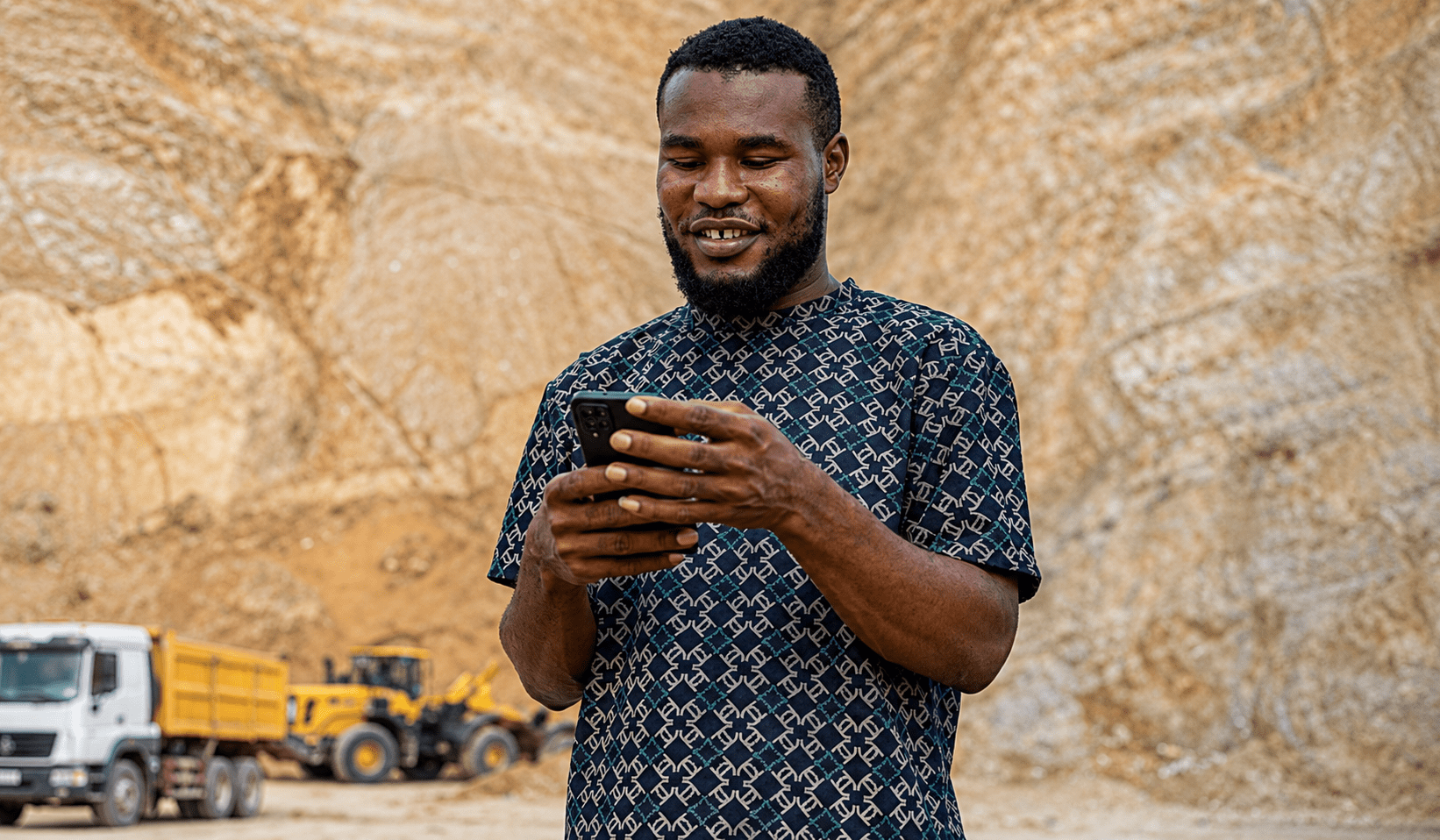

How A Smartphone Got Ghana’s Everyday Earners To (Finally) Trust Insurance

By Henry Nzekwe

|

May 21, 2026

Abraham, a construction worker in Ghana, had never held an insurance policy in his life. When a sudden illness landed him in hospital, he faced the difficult choice of missing work and losing income, or delaying treatment and risking his health.

What changed everything was a smartphone. When Abraham purchased his device through M-KOPA Ghana’s “More than a Phone” instalment plan in January 2025, he didn’t know it came bundled with hospital cash cover from Turaco. Months later, when sickness struck, the policy paid out, covering his hospital bills and providing daily cash to manage expenses during his recovery.

“I didn’t have an income during the days I was sick in the hospital. Because they covered my hospital bills, I had cash to take care of my daily expenses,” Abraham said, as detailed in M-KOPA Ghana’s latest impact report, released Wednesday.

Abraham is one of 556,000 Ghanaians who have accessed credit through M-KOPA since 2021, and part of a quiet revolution in how insurance reaches Africa’s low-income earners, according to the report, which found that 67% of insured customers accessed health coverage for the first time through M-KOPA’s partnership with Turaco.

For decades, selling insurance to Africa’s informal sector was considered a tough gig. Premiums were too high, distribution was too fragmented, and trust was virtually non-existent. Across the continent, insurance penetration remains at just 2.7% of GDP, which is less than half the global average of approximately 7%. In Ghana, where mobile technology now contributes GHC 94 B (~USD 8 B) to the economy, roughly 8% of GDP, millions remain locked out of formal protection.

M-KOPA is cracking the code by making insurance incidental. Individuals buy a smartphone on credit with the coverage baked in, eliminating the hurdle of shopping for a policy.

The January 2025 launch of “More than a Phone”, which bundles health insurance, affordable data, and device protection directly into every smartphone instalment, drove a fourfold surge in sales and expanded operations across all 16 regions of Ghana.

For many users, the services attached to the device now matter more than the device itself. Forty-four percent of customers accessed a formal product or service for the first time through M-KOPA, and 36% said their financed smartphone was the first phone they had ever owned.

“M-KOPA Ghana works to dismantle barriers to formal financial services, and this report shows what’s possible when Every Day Earners get access,” said Chioma D. Agogo, General Manager, M-KOPA Ghana.

“From first-time smartphone ownership to first-time health insurance, we’re proving that bundling meaningful services with connectivity changes what people can achieve.”

Forty-three percent of female customers said they chose an M-KOPA phone specifically for the health insurance, and 67% of insured customers now feel more confident handling health expenses, according to the report.

Before M-KOPA, 40% of insured customers relied on harmful coping mechanisms – borrowing money, selling assets, cutting back on food, or delaying treatment – to manage medical costs. Today, that vulnerability is being systematically dismantled, one smartphone at a time.

The model is now being replicated and scaled. Across M-KOPA’s five markets, the fintech is nearing 10 million customers and onboarding over 10,000 new users daily, according to a May 12 company announcement. Revenue grew more than 65% in 2024, with growth remaining profitable into 2025 and 2026.

Kenyan Court Kills ‘Rogue Employee’ Defence In Landmark Data Breach Ruling

By Staff Reporter

|

May 19, 2026

A Kenyan High Court ruling that ordered Safaricom to pay KES 9.9 M (USD 76 K) for a massive data breach has effectively killed the “rogue employee” defence, placing corporate Africa on notice that constitutional privacy obligations cannot be outsourced or delegated.

In a judgment delivered on May 13, Justice Bahati Mwamuye of the Constitutional and Human Rights Division found that the telecoms giant violated the rights of 11 subscribers whose personal and financial data, including betting histories, M-Pesa transaction records and geolocation information, was extracted by employees and sold to betting companies including Odibets between 2018 and 2019.

The breach compromised information belonging to more than 11.5 million subscribers, making it one of the largest known violations of subscriber privacy on the African continent.

Safaricom’s defence rested on what had previously been a reliable corporate shield, claiming rogue employees acted outside their authority. The company argued that because the individuals—including a manager of networks and M-Pesa systems who designed a bespoke algorithm to mine subscriber data—acted without authorisation, the institution itself should not bear constitutional responsibility.

The court rejected that argument entirely.

“The breach happened because of systemic failures inside Safaricom’s own infrastructure, poor data governance, weak internal oversight, and inadequate security controls,” the judgment found. “The rogue Safaricom employee could only do what they did because the system made it possible. That is on the company.”

Justice Mwamuye went further, ruling that Article 31 of Kenya’s Constitution, the right to privacy, imposes a “positive and non-delegable duty” on data controllers.

The court also found violations of Article 28, the right to dignity, and Article 46 on consumer protection, significantly expanding the definition of harm in data breach cases.

Under the ruling, a person whose data leaks does not need to demonstrate financial loss to have a valid claim. Reputational damage and psychological harm are sufficient.

Each of the 11 petitioners was awarded KES 900 K in general damages, with interest accruing from the date of judgment until payment in full. Safaricom was also ordered to bear the full costs of the petition.

But the real significance lies in what comes next. The court’s reasoning applies to every bank, telco, insurer, health provider and government body sitting on large volumes of personal data across the continent.

“If a breach happens and you cannot show clear documentation of who had access to what, what monitoring was in place, and how quickly you would have caught unusual activity, you are exposed,” the judgment warned. “The rogue employee story will not save you.”

Observers say the ruling establishes a binding precedent that will shape data protection litigation across Kenya and beyond.

Safaricom, which has not yet indicated whether it will appeal, is now staring down the barrel of cascading litigation. The court’s findings, that employees extracted and trafficked subscriber data to named betting firms over a sustained period, have opened the door for millions more affected subscribers to seek redress.