Micro-Lending In Africa: Which Model Is Going To Succeed? [Opinion]

Increasing access to finance is fundamental to the growth of small and medium enterprises (SMEs) and economic growth in Africa. Yet, access to credit is one of the main financial challenges that unbanked and low-income people face on the continent. Indeed, almost 70% of the population has limited access to credit and traditional banking services. This has led to innovations in the microcredit space that are pushing mobile financial inclusion forward.

Besides, the lack of credit bureaus providing accurate credit information is one of the major obstacles hindering micro-lending take-off in Africa. While financial inclusion is still low, the financial sector has a lot of momentum in Africa and attracts lots of capital — about 45% (~$253M) of all African ventures funding in 2017 went to financial inclusion. Technology is bringing fundamental transformation and opening up new opportunities to reach populations that were previously underserved.

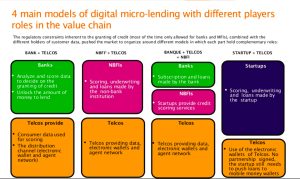

On the one hand, Fintech-based lenders like Branch ($84.7M), Tala ($109.4M), Jumo ($79.2M), OneFi ($13M) or Mines.io ($17.2M) are springing up and driving innovation in Sub-Saharan Africa. With just a phone and an internet connection, customers are now able to get a loan. They have the flexibility to provide faster access to credit through mobile apps, using AI algorithms that analyze alternative data such as phone records, bank records, mobile money and payment transaction history to assess credit risk for individual consumers or small businesses.

Source: Original Digital Ventures Report

On the other hand, more and more MNOs, traditional financial services providers (banks, microfinance institutions) and Fintech companies have begun engaging in partnerships to offer microloans (such as Jumo and MTN, Safaricom and Commercial Bank of Africa (CBA) to provide M-Shwari) around different models. MNOs have the distribution network (including mobile money agency network), licensed financial institutions have the client knowledge to develop specific products and Fintechs have the knowledge to build better credit risk models.

However, digital micro-lending in Africa still faces challenges despite the amount of capital available and exit opportunities in the financial sector. Part of the problem is the technical and integration challenge between banking systems and MNOs’ but also the inherent risks to this business — mostly capital, currency and regulatory. Many other challenges are hampering micro-lending.

How to educate borrowers to avoid debt burden? How to make loans more affordable and protect borrowers? What are the main business KPIs to look at before investing in micro-lending? What is the position of regulation on the data privacy?

– Key drivers of these innovations (technology platforms, type of credit scoring data, regulation, etc.);

– How Fintechs are leveraging the digital channel to create new models (existing versus new models);

– Upcoming trends: utilities lending (airtime, power, renewables etc.) are also on the rise. PYG and payment players offering digital loans options to their customers respectively in the form of upfront payment of solar kits or merchant cash advance (they will soon also be able to score customers when they reach a critical size in terms of adoption).

Featured Image Courtesy: Visual China

Marième Diop currently serves as a VC investor in early stage African startups at Orange Digital Ventures Africa – Orange Group’s 50m€ VC fund. This article first appeared here and is republished with permission.